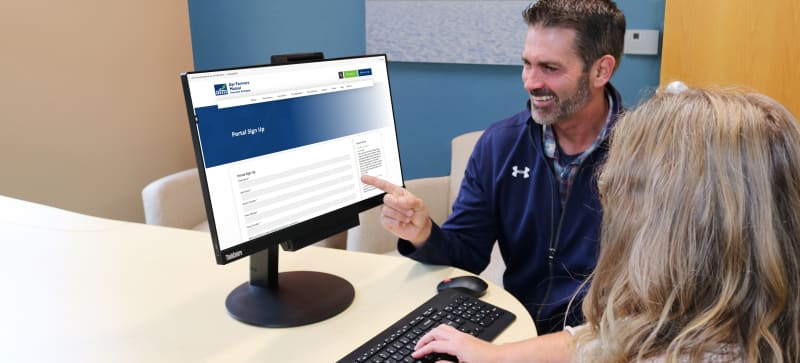

Your Insurance Documents, Your Way with the AFM Portal

Your Insurance Documents, Your Way - Introducing Paperless Delivery, through the AFM Portal

The Ayr Farmers Mutual Insurance Blog provides readers with valuable information, blogs, job postings, community involvement, and updates on everything you need to know about insurance in Ontario.

Your Insurance Documents, Your Way - Introducing Paperless Delivery, through the AFM Portal

Ayr Farmers Mutual Insurance Company is seeking a Loss Prevention and Building Maintenance Coordinator to join our team. View the job posting to learn more and to apply.

Ayr Farmers Mutual Insurance Company is seeking a Manager of Compliance & Customer Experience to join our team. View the job posting to learn more and to apply.

Ayr Farmers Mutual Insurance Company is seeking a Claims Administrator to join our team. View the job posting to learn more and to apply.

Ayr Farmers Mutual Insurance Company is seeking a Business Analyst to join our team. View the job posting to learn more and to apply.

We’re bringing free ice cream to five communities across southwestern Ontario, and pairing each stop with a local cause worth supporting. Five stops. Free ice cream. Good neighbours. Great cause.

Ayr Farmers Mutual celebrated 34 local organizations at its 2026 Volunteer Appreciation & Donation Night, honouring the volunteers who make our communities thrive.

Ayr Farmers Mutual was honoured with the 2026 OMIA Outstanding Contributor Award — the first Ontario Mutual to earn this honour twice.

Policyholders and Members are invited to AFM's Annual General Meeting, which is also a Special General Meeting.

Here's a home safety update you'll want to know about: new carbon monoxide alarm requirements took effect on January 1, 2026.

Please contact us and Get Started Today! One of our Agents will work steadfastly to provide you with the information you need. Just shopping around? No problem! Our Agents are happy to help provide you with information, so you can make the best decision—For You.